Warning: What the Super Reforms really mean for you in 2017 and beyond

From 1 July 2017, a number of changes to superannuation rules that were announced in the 2017 Federal Budget will take effect.

We’ve written this e-book for a number of reasons:

- Firstly: to help you understand what has changed in super.

- Secondly: there’s a lot of information out there about the super changes going around, but very little on how they’ll limit your ability to grow your retirement savings and retire with enough money.

- Finally: by providing you with a better understanding of the changes, you’ll hopefully re-assess your current financial strategy and consider whether additional investment strategies are needed to work side-by-side with your super to help you achieve your retirement savings goals.

While the government markets the super reforms as being part of a fairer system, it’s important to take a closer look- not only at what’s changed, but what’s being taken away from you as a result.

Hard-hitting facts about the 2017 super reforms:

- The primary purpose of the 2017 super reforms is to generate billions of dollars in extra revenue for the government by collecting more money from tax payers and their super funds.

- The 2017 super reforms significantly restrict the amount of money that you can contribute to super with both before and after-tax contributions.

- An additional super contributions tax has been introduced to a wider net of high-income earners who will have to pay more taxes on super contributions. Super reforms will result in a 100% increase in super contributions taxes for high-income earners

- The amount of tax-free earnings that you can gain to accelerate your investment earnings and growth in the super pension phase has now also been capped, which means more taxes will be payable.

- Most Australians will pay tens or even hundreds of thousands in additional taxes over their lifetimes as a result of the super reforms, which effectively reduces your retirement nest egg.

Who benefits most from the 2017 super reforms?

Contrary to how it’s pitching the changes, the government is the ultimate beneficiary, as you’ll realise when you read through this e-book.

Low-income earners making less than $40,000 benefit slightly. However, the benefits they’ll be entitled to, though better than nothing, won’t go far enough to help them retire with a lot more money.

Next steps, after reading all about the super reforms

If you’d like more information or would like to get in touch with a qualified super or wealth accountant to discuss how the super reforms will impact you and what you can do about it, call Tax Effective Accountants on 1300 399 839 today.

Speak to a wealth accountant todayMake an appointmentRequest a callback

Disclaimer

This e-book has been written by Tax Effective Accountants.

The information contained is general information only and does not take into consideration your personal financial situation, goals and obligations.

This e-book should not be used as a substitute for financial advice.

The new super reforms can be complex. So, if you’re considering making changes to your super strategy, we recommend that you talk to a qualified accountant or financial planner to help you determine the best super strategy for you.

Tax Effective Accountants assumes no responsibility for any actions you take without seeking professional advice.

Contents

- Introduction to the Super Reforms

- Disclaimer

- Contents

- Super is still super- what hasn't changed

- Changes to concessional contributions

- Concessional contribution limit slashed

- Concessional contribution catch-up provision

- Reduced high-income tax threshold (Division 293 tax)

- Removal of 10% test

- Opportunities prior to 1 July (concessional contributions)

- Changes to non-concessional contributions

- Non-concessional contribution limit slashed

- $1.6 million non-concessional contribution limit

- Increased spouse contribution tax offset threshold

- Opportunities prior to 1 July (non-concessional contributions)

- Introduction of $1.6 million pension transfer balance cap

- Transition to Retirement pension changes

- Temporary Capital Gains Tax relief for SMSFs

- Introduction of defined benefits pension cap

- Other changes to superannuation

- Low income super tax offset

- Anti-detriment payment abolished

- Where to from here?

- Book an appointment

Super is still super

Before getting into the details of the super reforms, it’s important to understand that superannuation is still the most tax effective vehicle to grow your retirement savings.

Benefits of super in a nutshell:

- Pre-tax super contributions will continue to be concessionally taxed at a maximum rate of 15%[1], not your marginal tax rate of up to 49%**, which means more of your money will be available for investment.

- Investment earnings in super are also taxed at a maximum rate of 15%, so that you’ll keep more money from your returns that’s reinvested back into your super, year after year.

- If you sell an asset in super that has grown in value, as long as you’ve held the investment for more than 12 months, your fund will pay no more than 10% in capital gains tax.

- When you retire and convert your super into a pension, taxes on your fund’s investment earnings and capital gains will drop to zero. Your pension payment should also remain free of tax, provided that you’re 60 years of age or over.

This allows you to multiply your return on investment and build up more money for your retirement with no additional risk.

[1] Individuals with incomes above $300,000 in 2016/17 will pay an additional 15% contributions tax on personal deductible and other concessional contributions. This threshold will reduce to $250,000 from 2017/18

** Including the Medicare Levy, and for 2016/17, the Temporary Budget Repair Levy of 2%, on taxable income exceeding $180,000

2017 Super Reforms at a Glance

Changes to concessional (pre-tax) super contributions

Concessional contribution limit slashed

Concessional contributions are your pre-tax contributions to super. They include:

- Your employer’s compulsory super guarantee

- Salary sacrifice amounts

- Additional employer contributions

- Personal deductible contributions made by self-employed Australians

From 1 July 2017, the amount of concessional contributions you can make per year will be slashed from $30,000-$35,000[1] to $25,000.

Note that if you’re aged between 65 and 74 years of age, you’ll need to meet a work test to be eligible to make concessional contributions into super.

What does this mean for you?

By reducing the amount of before-tax contributions that you can put into super:

- Your ability to increase your super falls because less money can be contributed and invested into super each year.

- You can contribute $5,000-$10,000 less in a the low-tax super environment - these amounts will now have to be received in cash, so you’ll be taxed on them at your marginal tax rate.

For most Australians, these rates range between 34.5% and 49%- compared to the contributions tax of 15% if the funds were contributed to super and taxed concessionally.

Example:

John is 50 years of age and earns $120,000 per annum. His employer contributes the compulsory 9.5% super guarantee ($11,400) to his super fund.

He has surplus cash flow and decides that he wants to accelerate his super savings so he can have enough money to retire on when he stops work.

In the 2016-17 financial year, he decides to salary sacrifice an additional $23,600 into super, bringing him up to the $35,000 concessional contribution limit. Rather than paying 39% (Medicare Levy inclusive) on his salary sacrificed contribution, he’ll only pay a 15% contributions tax on entry into his super fund. This saves John $5,664 in tax which is invested into his super fund.

From 1st July 2017, John can now only sacrifice $13,600, not $23,600. He’ll still save $3,264 in tax on the amount he put in super, which will increase his super balance and investable funds.

However, because the concessional contribution limit has been slashed by $10,000, it also means that he’ll now have to pay $3,900 in tax- as opposed to $1,500 if it were in super- on the $10,000 he can no longer salary sacrifice.

In other words, John will have to pay an additional $2,400 in income tax because of the reforms- but will still save more than if he didn’t contribute any funds into super.

[1] $30,000 if you’re below 49 years of age; $35,000 if you’re aged 49 or above

Catch-up unused concessional contributions

The government has provided a consolation prize for the reduction to the concessional contribution limits.

If you contribute less than the $25,000 limit during the financial year from 1 July 2018, you can add the unused amount to your limit for the next year. These unused amounts can be accumulated on top of each other for up to 5 years.

But there’s a catch. That is, the catch-up provision can only be used if your super balance is below $500,000.

Example:

On 30 June 2019, Mary has a total super balance of $390,000. She has an unused cap of $7,500 in 2017/18 and $15,000 in 2018/19.

Since only unused concessional caps amounts from 2018-19 can be carried forward, Mary can increase her concessional cap for 2019-20 by $15,000 to $40,000.

If she doesn’t reach the limit during the 2019-20 year, it can be rolled over to the next year- she can keep rolling the unused amounts over for 5 years in total.

Pros and cons of the catch-up provision:

- The good news is that from 1st July 2019 you’ll be able to increase your concessional super contributions

- However, the reality is that with an increasing cost of living, higher rents and debt repayments thanks to significant home loans, not too many Australians have the excess cash to fully utilise this provision

Reduction in high income contributions tax threshold – Division 293 Tax

From 1st July 2017, the high-income contributions (or Division 293) tax threshold has been reduced from $300,000 to $250,000.

Essentially, the government has significantly increased the number of taxpayers who will have to pay the extra 15% high-income contributions tax on top of the general 15% contributions tax.

So, you may now be liable to pay the Division 293 tax, even if you weren’t before.

The problems:

- If you earn $250,000 or more, your super taxes will go up by up to 100%- so 100% more will be taken out of your super contributions.

- You’re not only losing thousands of dollars- you’re losing the opportunity to reinvest these funds and make big returns over time.

The total loss to your super balance as a result could come up to tens of thousands of dollars, if not more.

Example:

Rick is an IT director earning $280,000. His employer contributes $25,000 to his super each year.

- Before 1st July 2017, Rick would only have had to pay the general super contributions tax of 15%, or $3,750.

- After 1st July 2017, Rick will not only be liable to pay $3,750 in the general super contributions tax, but also an additional higher income contributions tax of 15%, increasing the amount of tax his super will pay by $3750, or 100%, for a total of $7500.

- Over 10 years, this could cost Rick $37,500 in additional taxes, plus any investment earnings lost as a result.

Removal of the 10% test for deductible super contributions

Prior to 1 July 2017, if you were predominantly or partially self-employed, you could only get a tax deduction on your super contributions if less than 10% of your total income earned was from employment income.

This rule has been scrapped, which means that you can now make a personal tax deductible super contribution regardless of how much you earn from any source.

The same concessional contribution limits apply- you can contribute $25,000 maximum from 1 July 2017.

The good news with the removal of the 10% test:

- It should encourage more self-employed people to make concessional super contributions so they can reduce their taxes and grow their retirement balance.

- If your employer doesn’t allow you to salary package, you can now make a personal tax deductible contribution yourself without having to rely on your employer

Concessional contribution opportunities prior to 1 July 2017

You do have an opportunity to grow your super before 1 July 2017- if you start today.

Maximise concessional contributions

In the current financial year, your contributions are capped at a higher level. That’s $30,000 for anyone under 49 years of age, and $35,000 for anyone 49 years and over.

If your cash flow allows for it, you should definitely consider taking advantage of the higher contribution limits that are valid until the 30th June 2017- a little can go a long way when it comes to boosting your wealth in super.

Speak to a wealth accountant todayMake an appointment >Request a callback >

Changes to non-concessional (after-tax) super contributions

Non-concessional contribution limit slashed

Non-concessional contributions are your after-tax contributions to super. They include after tax income from wages, savings, spouse super contributions and after-tax proceeds from the sale of investments.

The annual non-concessional contribution limit will be slashed by 44.44%, from $180,000 to $100,000.

This limit will be indexed at $10,000 increments annually- that is, it’ll increase by approximately $10,000 each year.

Note that if you’re aged between 65 and 74 years, you will need to meet a work test to be eligible to make non-concessional contributions into super.

3 year bring-forward provision for non-concessional contributions

As a result of the reduction in the contribution limit, the maximum non-concessional contribution amount that can be brought forward over three years from 1 July 2017 has also reduced by $240,000 from $540,000 to $300,000.

So if you contribute even a cent over $100,000 in non-concessional contributions, you trigger the bring-forward provision for three years. This means that you can’t make contributions that total over $300,000 for three-years. This includes the year you made the contribution.

Why the reduced non-concessional contributions threshold is a problem for you

- Like the reduced concessional contributions cap, it significantly reduces your potential to increase your super balance because it decreases how much you can invest within the low-tax super environment and accelerate your returns.

- If you’ve sold investments or received an inheritance or significant bonuses, you’ll only be able to contribute a maximum of $300,000 of the proceeds into your super over three years. This is $240,000 less, or over 4 years, $480,000 less under the new super reforms.

- If you had a family super fund with you and your spouse, this would effectively reduce the amount you can contribute as a family by $480,000 in one year and $960,000 over 4 years.

- With the reduced contribution limit, any surplus funds that you have that cannot be invested into super will have to be invested another way, for example in your own name, joint names, a company or a family trust.

- Future capital gains taxes can also go from nil when your super’s in the pension phase, to significant when taxed at company or marginal tax rates.

Regardless of which structure your funds are invested in, the tax rate on the non-super investments generally range anywhere between 30% and 49%- much higher than the 15% super tax rate.

This is a big reduction in net investment returns and your potential growth.

This is a large blow to anyone who was planning to sell assets in the future and contribute the proceeds into super to enjoy the reduced taxes, including the tax-free status on super pensions.

Example:

Ronald and Jane are both 50 years of age.

Ronald earned an income of $120,000 and Jane $82,000 per annum.

Ronald’s mother passed away and left him her family home. After selling the home he was left with $1,450,000.

Realising that they haven’t got enough money in super, he decides to make a non-concessional contribution into their super with the profits.

Under the old rules – pre-1 July 2017

Under the old rules, Ronald would have been able to make two $180,000 after-tax contributions- one for himself and one for Jane- in the current financial year (totalling $360,000).

The following financial year, he could have used the 3-year bring forward provision and contributed $540,000 each for himself and Jane ($1,080,000 total).

That’s approximately $1,440,000 being put into their super in less than 12 months. This would then be invested in a low-tax environment where investment earnings are taxed at a maximum of 15%.

Any capital gains achieved on the selling of assets held in super, provided the assets were held for more than 12 months, would only be taxed at a maximum of 10%.

Under the new rules – from 1 July 2017

Under the new super rules, Ronald would be limited to making an after-tax contribution of $100,000 for him and Jane in the current financial year, and within 12 months, additional after-tax contributions of $300,000 each by applying the 3 year bring forward provision.

So, he could only contribute approximately $800,000 into super for himself and Jane.

Impact of the new rules

Under the new super rule, Ronald can contribute $640,000 less into super.

That’s a huge difference.

It’ll also cost Ronald and Jane tens of thousands of dollars more in taxes each year because that $640,000 would have to be invested in either their personal names, a company or a family trust, where it would be taxed at anywhere between 30% and 49%.

Result when in the super accumulation phase:

- Ronald and Jane will pay 100-227% more in income tax taxes per annum.

- Less money will be available for reinvestment which could add tens or even hundreds of thousands of dollars in additional tax liabilities, that otherwise could have been saved and reinvested into super.

- Let’s say that over the years their $640,000 investment doubled in value, then the asset was sold.

The $640,000 capital gain would attract anywhere between $96,000 to $156,000 in capital gains taxes if the asset was held outside of super.

If the asset was held inside of super, the maximum capital gains tax liability would be $32,000. Hence, Ronald and Jane could pay an additional $64,000 to $124,000 in capital gains taxes as a result of the super reforms.

Result when in the super pension phase:

- If the assets were held in the pension phase, income or dividend earnings would have been tax-free- meaning tens of thousands of dollars more could have been reinvested into super.

- No capital gains tax would’ve been payable under the old rules. Under super reforms, Ronald and Jane could pay between $96,000 and $156,000 more in capital gains taxes if the assets had to be held outside of super.

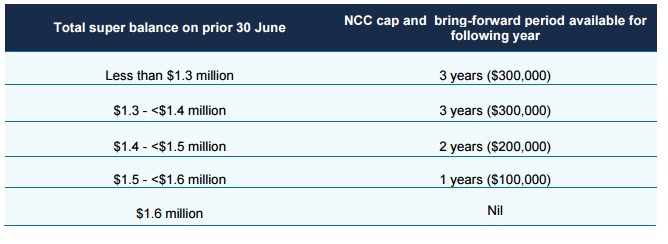

Introduction of $1.6 mill limit for non-concessional contributions

If the reduction in the annual non-concessional contribution limit wasn't enough, a $1.6 million super balance cap has also been introduced.

What this means is that if your super balance on 30 June is $1.6 mill or more, you won’t be able to make any non-concessional contributions what so ever.

And if you’re approaching a $1.6 million super balance, but aren’t quite there yet, then your number of years of bring-forward provisions will also go down.

Here's a table to give you a better indication.

Example:

Rebecca is 61 years of age and wants to make a non-concessional contribution to increase her super.

She has $1,450,000 in her super balance on 30 June 2016 and wants to know how much money she can contribute after tax to her super.

Assuming that Rebecca has made no non-concessional contributions in the past three years and based on the table above, Rebecca would be limited to making a maximum non-concessional contribution of $200,000- only 2 years’ worth of contributions.

If she made the contribution before 30 June 2017, she could have made a maximum of $540,000 in non-concessional contributions.

That’s $340,000, 70% more in contributions.

Problem with the $1.6 mill limit for non-concessional contributions

This accelerates all the problems mentioned above in the new non-concessional limits section because it puts in an additional hurdle that reduces your ability to contribute money into super if you have a higher super balance.

Increase in spouse contribution tax offset threshold

Prior to 1 July 2017, if your spouse earns an assessable income (including reportable fringe benefits and reportable super contributions) of under $13,800, you could claim a tax offset 18% for non-concessional contributions to their super of up to $3,000 per annum.

The new threshold has increased from $13,800 to $37,000.

In other words, if your spouse’s assessable income is below $37,000, you’ll be eligible for a maximum tax offset of $540.

If your spouse’s assessable income exceeds $39,999, you won’t receive a tax offset at all.

However, if your spouse earns between $37,000 and $40,000, you’ll be able to claim a partial tax offset.

Benefits of the increase in spouse contribution tax offset threshold

- More Australians will qualify to claim a tax offset, which will help encourage people to make non-concessional contributions to their lower income earning spouse’s super account.

- This will also help increase your spouse’s super balance, which may have been diminishing because of super fees and insurance premiums

Non-concessional contribution opportunities prior to 1 July 2017

You do have an opportunity to grow your super before the reforms take place on 1 July 2017 and severely restrict your super investment and earnings. But only if you act fast.

Maximise non-concessional contributions

If you have cash you’d like to contribute to super or assets you’re selling prior to 30 June 2017, you may want to take advantage of the higher non-concessional contribution cap, so long as you meet the criteria.

It’s best to start immediately, so that you can give yourself a head start before the reforms take effect.

Speak to a wealth accountant todayMake an appointment >Request a callback >

$1.6 mill pension transfer balance capped

Tax-free status on investment earning in super pensions has been limited

Prior to 1 July 2017, if you converted your super to an account-based pension, all interest, dividends and capital gains taxes earned in your fund would have been tax-free- regardless of the balance.

This made superannuation incredibly attractive to high net worth individuals. They’d often sell businesses, investment assets, and sometimes transfer assets, through self-managed super funds to take advantage of tax-free status on super pensions.

From 1 July 2017, a pension transfer cap will apply to both new and existing super balances of more than $1.6 million.

This means that only $1.6 million dollars can be rolled over into a super pension and obtain the tax-free treatment on fund earnings.

Any surplus funds over $1.6 mill will either:

- Have to stay in the super accumulation phase, and be taxed at 15% on income and 10% on capital gains (for assets that were sold and owned for 12 months or more)

- Be cashed out of super altogether

The right option is the one that provides you with the best tax outcome.

This cap is applied per person, so if you have a self-managed super fund with multiple members, each member has their own personal $1.6 mill pension transfer cap.

Note that this is a lifetime limit and will be indexed annually in $100,000 increments, or go up by around $100,000 a year.

Transitional rule for existing excess transfer balances

If you’re over the transfer balance cap on 30 June 2017 by less than $100,000, the excess amount will be disregarded for up to 6 months. If you don't remove the excess before the 6 months is over, it'll be taxed on its earnings at a maximum 15% tax rate.

If you’re over the balance transfer cap by more than $100,000, you won’t have a 6-month transition period- you’ll need to have rolled over the excess amount prior to 1 July 2017.

What about defined benefits schemes?

Not all super income streams have an account balance. This can be the case with some defined benefits schemes.

In this case, the account balance will be calculated as the annual income the fund will pay as an income times 16.

Example:

On 30 June 2017 Veronica is in receipt of a capped defined benefit pension which pays her a lifetime pension of $3,000 per fortnight.

The value of Veronica’s pension for the purposes of the transfer balance cap is calculated as follows:

Annual income the fund pays = ($3000/14) × 365 = $78,214

Pension value = $78,214 × 16 = $1,251,430

Veronica’s defined benefits scheme is below the $1.6mill cap.

The problem with the $1.6 million pension balance transfer cap

- All existing super pensions with more than $1.6 mill balances as at 30 June 2017 will be forced to roll over the excess amounts back into a super accumulation account or cash it out

- Australians with high super balances have no choice but to pay additional yearly taxes that can range from anywhere from a few dollars to tens or hundreds of thousands of dollars, depending on the balance and future capital gains

Should I still consider super pensions?

Absolutely. Even though a pension balance transfer cap has been introduced, you definitely shouldn’t assume that super pensions are no longer an attractive option.

The pension balance transfer cap doesn’t change the fact that:

- Regardless of the pension transfer limit, super may still work out to be the best place to park large chunks of your wealth

- Paying concessional taxes on investment earnings in the accumulation phase might not be as good as paying no tax, but can still be much better than paying tax at your marginal tax rate for high net worth individuals.

- Pulling money out of the accumulation phase once you have turned 60 years of age is still tax-free, regardless of whether the money is taken out of the pension or accumulation phase.

- The tax-free status on pension payments still remains tax free after reaching the age of 60.

Example:

Prior to 1 July 2017, Tom retired at the age of 60. He had a super pension balance of $3,000,000 and was drawing out the minimum pension of $120,000 (4%), from it, tax-free.

All the earnings in his super fund were tax-free.

Let’s assume that his balance on the 30 June 2017 was still $3,000,000.

Tom would only be permitted to keep $1.6 mill in his super pension account. The remaining $1.4 mill would either need to be rolled back into an accumulation super fund or cashed out of super completely.

He’ll still be able to draw out any income over the minimum required by law.

Assume that he keeps the money in super.

The earnings on his super pension will remain tax free, however this is not the case with the $1.4 mill that will be rolled back into the accumulation phase.

Let’s assume that Tom earns a 5% income, approximately $70,000. He’ll have to pay a maximum tax rate of 15% on his earnings- $10,500.

So, as a result of the pension transfer cap, the government will raise an additional $10,500 a year from Tom’s accumulation fund. This process will be repeated for as long as Tom is alive and has money in his accumulation fund.

Hence, as a result of the super reforms, Tom will lose tens or even hundreds of thousands in taxes throughout the remainder of his lifetime.

We haven’t factored in future capital gains taxes, but we’re sure you get the drift.

Transition to Retirement (TTR) Pension changes

TTR investment earnings tax-exemption removed

Just in case you’re unsure of what a transition to retirement pension is, let’s quickly take a step back.

A transition to retirement strategy is a strategy that allows working Australians aged 55 or over to salary sacrifice money into super and replacing it with tax-free or partly tax-free income from their super pension.

To qualify, you just need to be at or above the preservation age of 55 years.

But there are limits to how much you can draw out in pension payments from your super. The minimum amount is 4% and the maximum is 10%.

- If you’re aged 60 years and above, your super pension payments are tax-free

- If you’re between 55 and 59 years of age, your super pension payments are made up of both taxable and tax-free components.

The taxable component is taxed at your marginal tax rate minus a 15% tax offset, and the tax-free component remains exactly that- tax-free.

All investment income and capital gains are also free from tax.

How have the super reforms changed TTRs?

From the 1st July 2017, you’ll no longer be tax-exempt on investment earnings from your TTR super pension.

These new rules apply to both new and existing TTR arrangements.

Note that the taxation of the income payments from TTR pensions will not change. Income payments will continue to be tax-free from age 60.

The taxable portion of income payments for those aged 55-59 will be taxed at your marginal tax rate minus a 15% tax offset.

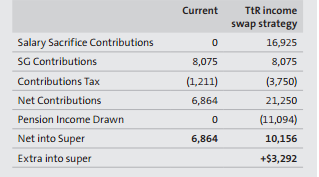

Example:

Colin is 60 years of age and works full time. He earns an income of $85,000 p.a. After-tax, he receives a net income of $64,128.

His employer pays 9.5% of his salary into super ($8,075) and he has a super balance of $250,000.

Colin doesn’t have any spare income to make extra super contributions.

He can use the TTR income swap strategy:

We know that Colin can draw a super pension income of between 4 and 10%. That’s between $10,000 and $25,000.

Colin’s concessional contribution limit after the 1st July 2017 is $25,000, and his employer already contributes $8,075, which means he can salary sacrifice $16,925 into super without exceeding his limit.

If Colin hadn’t contributed that $16,925 into super, he’d be taxed at his marginal rate and be left with $11,094.

So to maintain a net income of $64,128, he’d need to salary sacrifice $16,925 into super and replace it by drawing out $11,094 by drawing a transition to retirement stream income from his super.

The benefit of the TTR strategy is a risk-free return of $3,292 which is added to his super and invested in a concessionally taxed environment.

Over 5 years this would equate to a risk-free return of about $19,645 plus earnings.

If you’re really interested in how the $3,292 benefit is calculated, here is a table to illustrate.

Negative impact of super reforms on TTR pensions for people aged 55-59

- The tax benefit of a TTR strategy if you’re under the age of 60 is now marginal at best, unless you have a very large tax-free component in your TTR income stream

- The reduction of the concessional contribution cap to $25,000 will further reduce the benefit of a TTR strategy, particularly if you’re aged between 55 and 59. In some cases you can even be worse off.

- Your earnings on assets held in the pension phase will be taxed at a maximum of 15%, which will put the brakes on the fund’s growth potential

Impact for clients aged 60 years and over

- The tax benefits of a TTR strategy if you’re 60 years or over, although diminished, still provide you with a risk-free tax benefit

Temporary Capital Gains Tax (CGT) relief for SMSFs

Transitional CGT relief

As a result of the $1.6 million pension transfer cap, if your existing super pension balance (account-based or transition to retirement pension) exceeds the cap, some assets in the pension phase will need to be returned to the accumulation phase.

The disposal of one or multiple assets would occur, creating a potential capital gains event.

The super reform measures have introduced a CGT relief provision to help lessen the potential CGT impact of this happening.

This will only apply to assets that a trustee has been required to transfer back to the accumulation phase due to the transfer balance cap and transition to retirement rule changes.

It’ll only be valid between November 2016 and 1 July 2017.

The provision will reset the total costs of acquiring and holding the assets- called the “cost base-“ to their current market value so that any capital gains you make are tax-free.

Because these costs are reset, the 12-month period you need to hold the assets for to access the capital gains tax discount also restarts.

The CGT transitional rules are complex and whether or not the fund should choose to apply the relief will depend on the fund’s circumstances.

If your SMSF needs to transfer assets from the pension phase back to the accumulation phase, seek professional advice immediately.

Example:

Max and Jenny have an SMSF. The fund holds assets that support Max’s $2.6 million super pension income stream, and separate assets to support Jenny’s accumulation interests.

To comply with the transitional rules, on 1 March 2017, Max partially transfers $1 million of his super pension assets back into the accumulation phase.

The cost base, or his costs of acquiring the assets was $750,000, meaning that they’d made an unrealised capital gain of $250,000.

So that this gain isn’t taxed, Max must record this choice when they submit the 2016/17 income tax return of the fund to obtain the CGT relief.

When the transitional CGT relief is applied, the asset is considered to have been purchased on 1st March 2017 at its $1 million market value, making the capital gain tax-free.

The 12-month period for the asset to be eligible for the capital gains discount is also reset to start on 1st March 2017.

Introduction of a defined benefits pension cap

Tax treatment of pension payments from capped defined benefit income streams

To ensure equal tax treatment of defined income streams and other types of retirement phase income streams, a separate defined benefit income cap of $100,000 per annum will apply.

That is, defined benefit pension payments over $100,000 per annum will be subject to additional taxation, depending on whether they’re from a taxed or untaxed pension.

Pension payments from taxed sources

If you receive a defined benefits pension that’s made up of taxed sources (including tax-free components), where payments exceed the defined benefit income cap of $100,000, 50% of the excess payment will be included in your assessable income and taxed at your marginal tax rate.

Pension payments from untaxed sources

If you receive a defined benefits pension that’s made up of untaxed sources, the entire payment will continue to be included in your assessable income and taxed at your marginal tax rate- but you’ll be entitled to a 10% pension tax offset.

If these payments exceed the defined benefits pension cap of $100,000, the excess amounts will also be included in your assessable income and taxed at your marginal rate, but the 10% pension tax offset will be removed.

Example:

Marcus is 61 years of age and receives a capped defined benefits pension of $170,000 per annum, all from taxable sources. Marcus also has multiple investment properties that pay him a net income of $50,000 per annum.

In this case, the following tax treatment would occur:

- The first $100,000 will be tax-free

- With $70,000 remaining in excess, 50% ($35,000) would be included in Marcus’s assessable income and taxed at his marginal rate

As a result, under the new super reforms, Marcus would be liable to pay an additional $12,325 in taxes on the $35,000 that exceeded the defined benefit pension cap.

No taxes would have been payable prior to 1 July 2017.

Impact of the defined benefits pension cap

- If you’re in receipt of a defined benefits pension that exceeds the $100,000 cap, your net cash flow will fall due to the new taxes under the super reforms

- The more income you earn from investments outside of your pension, including realised capital gains, the higher your assessable income and marginal tax rate. This can result in higher taxes being paid on your pension.

Speak to a wealth accountant todayMake an appointment >Request a callback >

Low income super tax offset

The low income super contribution will be abolished from 1 July 2017.

From that date, it’s being replaced by a low-income superannuation tax offset, which basically does the same thing.

This offset refunds you back the taxes you paid on your concessional (pre-tax) super contributions, such as employer contributions, if you’re a low-income earner with an adjustable taxable income of $37,000 or less.

Your adjusted taxable income includes your taxable income, reportable super contributions, reportable employer contributions, tax-free government benefits or pensions, deductible personal super contributions and net investment losses.

The low-income super tax offset will be paid by the government directly into your super fund. The maximum amount that will be contributed back into your fund is $500.

Example:

Martha earns an income of $35,000. Her employer makes compulsory super guarantee contributions of 9.5% ($3,325).

Martha’s super fund will deduct a 15% tax on the $3,325 concessional contribution. That is, it will take out $498.75 in contributions tax.

Because Martha makes less than $37,000, the government puts $498.75 back into Martha’s super fund.

Anti-detriment payment abolished

Anti-detriment payments have a significant impact on your loved ones in the case of you passing. From 1 July 2017, they’ll be abolished.

What is an anti-detriment payment?

On 1 July 1988 the federal government introduced a 15% tax on super contributions. To compensate for this, the government also reduced the tax on super lump sum payouts by 15%.

This new tax meant they’d now be getting less money than they otherwise would have been entitled to.

To make up for this, a voluntary “anti-detriment’ scheme was introduced, which was designed to refund the total amount of contributions tax paid by the super member during their lifetime to their beneficiaries.

Example:

Jonathan made contributions to his super totalling $200,000 and paid $30,000 in contributions tax over his lifetime. If Jonathan passed away now, his beneficiaries would be left with $170,000 plus earnings.

In other words, there would be a $30,000 detriment.

Under the anti-detriment scheme, the super fund has the option to pay the additional $30,000 to Jonathan’s beneficiaries as well as claim a tax offset on that amount.

Impact of removing the anti-detriment payment

By getting rid of anti-detriment payments, potential death benefit beneficiaries will receive tens of thousands of dollars more in additional death benefits.

Sharing is caring!

Do you have any like-minded family or friends that would appreciate or enjoy reading this e-book about the super reforms?

Share this e-book using your preferred social media button below.

Where to from here? Next steps.

Now that you really understand the new super reforms, you can see that the government’s put major restrictions on your ability to grow wealth tax effectively with your super.

You should start considering whether these reforms impact you enough for you to be rethinking your investment strategy and whether your current one’s still enough.

So, have a serious think about what you want to achieve financially.

Think about your current tax, financial super strategy and ask yourself, is what you’re doing enough?

- Will you have enough assets to live the lifestyle you want both before and after you retire?

- What will your life look like if you don’t achieve financial security?

Then make an appointment to talk to your trusted wealth accountant of financial adviser to discuss your options.

If you don’t have an adviser you trust:

Schedule your free financial health diagnostic valued at $395 with a Tax Effective wealth accountant who will help you:

- Navigate the complex, ever-changing world of super

- Review your current super, tax and financial situation

- Determine whether what you’re doing is enough

- Consider tax and financial strategies, such as:

- Buying property through super

- Gearing to invest in shares, direct residential or commercial property

- Setting up a self-managed super fund

- Getting into business

- Tax effective debt reduction strategies

- Super and personal tax minimisation

- And more

If you don’t live in Sydney or can’t make it to our Sydney CBD office, that’s okay, we service clients all around Australia via Skype.

E-Book Navigation

Share E-Book with friends